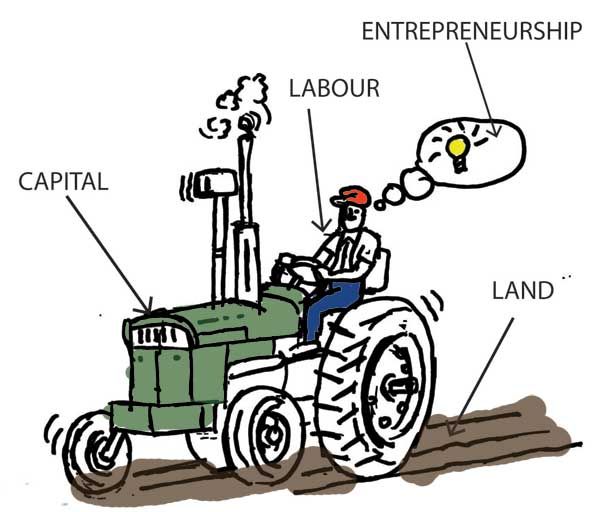

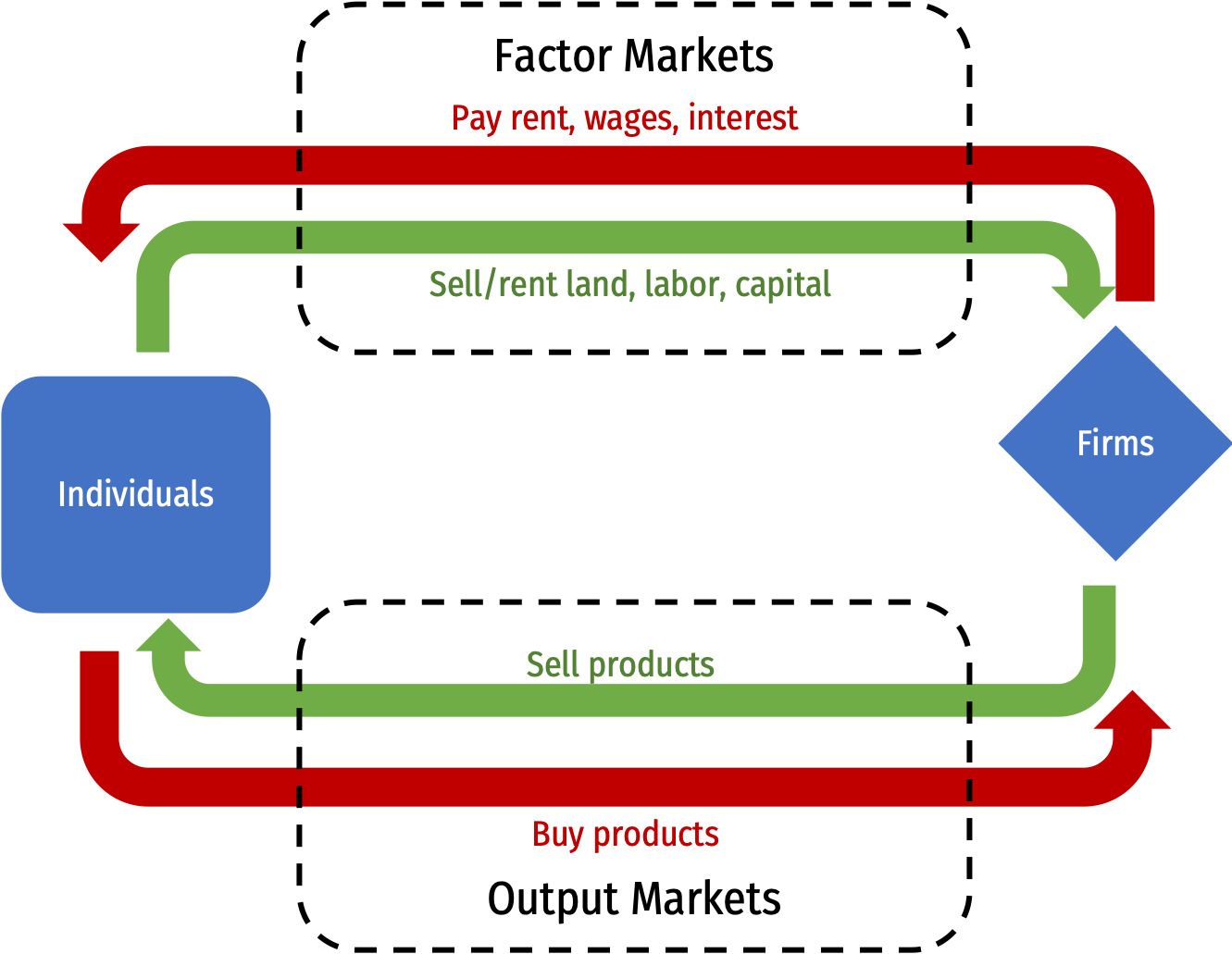

class: title-slide # 2.1 — Production and Firms ## ECON 306 • Microeconomic Analysis • Spring 2023 ### Ryan Safner<br> Associate Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/microS23"><i class="fa fa-github fa-fw"></i>ryansafner/microS23</a><br> <a href="https://microS23.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>microS23.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Production, Specialization, & Comparative Advantage](#7) ### [What Do Firms Do?](#33) --- # Producer Behavior .pull-left[ - How do **producers** decide: - which products to produce - in what quantity - using which inputs - and sold at what price? - Answers to these questions are building blocks for .hi-red[supply curves] ] .pull-right[ .center[  ] ] --- # The Basics of Production .pull-left[ - Nearly all goods must be **produced** before we can exchange & consume them - .hi[Consumption] is the **using up** of value to gain utility - .hi-purple[Consumption is the ultimate goal of all economic activity] ] .pull-right[ .center[  ] ] --- # The Basics of Production .pull-left[ - .hi[Production] is the **creation** of value, by transforming *lower*-valued goods (resources, inputs, etc) into *higher*-valued goods (outputs, consumer products, etc) - Iron Ore `\(\rightarrow\)` Steel `\(\rightarrow\)` Buildings, Bridges, Ovens, Water Bottles ] .pull-right[ .center[  ] ] --- # It's Demand all the Way Down! .pull-left[ - .hi-red[Supply] is actually .hi-blue[Demand] in disguise! - An .hi[(opportunity) cost] to buy (scarce) inputs for production because **other people** .hi-blue[demand] those same inputs to consume or produce **other valuable things**! - Price necessary to **pull them out of other valuable productive uses** in the economy! ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # What Do Firms Do? --- # The Firm .pull-left[ - In modern market economies, most production takes place in an organization known as a .hi[firm] - A legal fiction for particular purposes - It does not *have* to be this way, and for most of history it was not this way! - Craft guilds - Independent artisans - Independent contractors ] .pull-right[ .center[  ] ] --- # If Markets Are So Great, Why Do Firms Exist? .pull-left[ .smallest[ - Firms exist in the forms they do because they are .hi-turquoise[an efficient response to particular problems of economic organization] - Lots of interesting & Nobel-prize winning analysis - For now, we'll sidestep these and just *assume* firms exist. Learn more in my .hi[Industrial Organization] course: - [Why Are There Firms?](https://ios20.classes.ryansafner.com/class/3.1-class/) - [The Firm as Nexus of Contracts](https://ios20.classes.ryansafner.com/class/3.2-class/) - [Asset Specificity and Vertical Integration](https://ios20.classes.ryansafner.com/class/3.3-class/) - [Contractual Restraints & Property Rights](https://ios20.classes.ryansafner.com/class/3.4-class/) ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? I .pull-left[ - We'll assume “the firm” is the agent to model: - So what do firms do? - How would we set up an optimization model: 1. **Choose:** .hi-blue[ < some alternative >] 2. **In order to maximize:** .hi-green[< some objective >] 3. **Subject to:** .hi-red[< some constraints >] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? II .pull-left[ .smaller[ - Firms convert some goods to other goods: ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? II .pull-left[ .smaller[ - Firms convert some goods to other goods: - **Inputs**: `\(x_1, x_2, \cdots, x_n\)` - <span class="green">**Examples**: worker efforts, warehouse space, electricity, loans, oil, cardboard, fertilizer, computers, software programs, etc<span> ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? II .pull-left[ .smaller[ - Firms convert some goods to other goods: - **Inputs**: `\(x_1, x_2, \cdots, x_n\)` - <span class="green">**Examples**: worker efforts, warehouse space, electricity, loans, oil, cardboard, fertilizer, computers, software programs, etc<span> - **Output**: `\(q\)` - <span class="green">**Examples**: gas, cars, legal services, mobile apps, vegetables, consulting advice, financial reports, etc<span> ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? III .pull-left[ - .hi[Technology] or a .hi[production function]: rate at which firm can convert specified **inputs** `\((x_1, x_2, \cdots, x_n)\)` into **output** `\((q)\)` `$$q=f(x_1, x_2, \cdots, x_n)$$` ] .pull-right[ .center[  ] ] --- # Production Function as Recipe .pull-left[ .center[The production function  ] ] .pull-right[ .center[The production algorithm  ] ] --- # Factors of Production I `$$q=A \,f(t,l,k)$$` .pull-left[ .smaller[ - Economists typically classify inputs, called the .hi[“factors of production” (FOP)]: <table> <thead> <tr> <th style="text-align:left;"> Factor </th> <th style="text-align:left;"> Owned By </th> <th style="text-align:left;"> Earns </th> </tr> </thead> <tbody> <tr> <td style="text-align:left;"> Land (t) </td> <td style="text-align:left;"> Landowners </td> <td style="text-align:left;"> Rent </td> </tr> <tr> <td style="text-align:left;"> Labor (l) </td> <td style="text-align:left;"> Laborers </td> <td style="text-align:left;"> Wages </td> </tr> <tr> <td style="text-align:left;"> Capital (k) </td> <td style="text-align:left;"> Capitalists </td> <td style="text-align:left;"> Interest </td> </tr> </tbody> </table> ] .smallest[ - `\(A\)`: .b["total factor productivity"] (ideas/knowledge/institutions) ] ] .pull-right[ .center[  ] ] --- # Factors of Production II `$$q=f(l,k)$$` .pull-left[ - We will assume just two inputs: labor `\(l\)` and capital `\(k\)` <table> <thead> <tr> <th style="text-align:left;"> Factor </th> <th style="text-align:left;"> Owned By </th> <th style="text-align:left;"> Earns </th> </tr> </thead> <tbody> <tr> <td style="text-align:left;"> Labor (l) </td> <td style="text-align:left;"> Laborers </td> <td style="text-align:left;"> Wages </td> </tr> <tr> <td style="text-align:left;"> Capital (k) </td> <td style="text-align:left;"> Capitalists </td> <td style="text-align:left;"> Interest </td> </tr> </tbody> </table> ] .pull-right[ .center[  ] ] --- # What Does a Firm Maximize? .pull-left[ - We assume firms .hi-purple[maximize profit `\\((\pi)\\)`] - Not true for all firms - <span class="green">**Examples**: non-profits, charities, civic associations, government agencies, criminal organizations, etc</span> - Even profit-seeking firms may also want to maximize *additional* things - <span class="green">**Examples**: goodwill, sustainability, social responsibility, etc </span> ] .pull-right[ .center[  ] ] --- # Profits Have a Bad Rap These Days .center[  ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** ] .pull-right[ .center[  ] ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** - Suppose firm sells **output** `\(q\)` at price `\(p\)` ] .pull-right[ .center[  ] ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** - Suppose firm sells **output** `\(q\)` at price `\(p\)` - It can buy each **input** `\(x_i\)` at an associated price `\(p_i\)`, i.e. - labor `\(l\)` at wage rate `\(w\)` - capital `\(k\)` at rental rate `\(r\)` ] .pull-right[ .center[  ] ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** - Suppose firm sells **output** `\(q\)` at price `\(p\)` - It can buy each **input** `\(x_i\)` at an associated price `\(p_i\)`, i.e. - labor `\(l\)` at wage rate `\(w\)` - capital `\(k\)` at rental rate `\(r\)` - The profit of selling `\(q\)` units and using inputs `\(l,k\)` is: ] .pull-right[ .center[  ] ] --- # Who Gets the Profits? I .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` ] .pull-right[ .center[  ] ] --- # Reminder from Macroeconomics: “The Circular Flow” .center[  ] --- # Who Gets the Profits? I .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` - .hi-purple[The firm's costs are all of the factor-owner's incomes!] - Landowners, laborers, creditors are all paid rent, wages, and interest, respectively ] .pull-right[ .center[  ] ] --- # Who Gets the Profits? I .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` - Profits are the .hi-purple[residual value] leftover after paying all factors - Profits are income for the .hi[residual claimant(s)] of the production process (i.e. **owner(s)** of a firm): - Entrepreneurs - Shareholders ] .pull-right[ .center[  ] ] --- # Who Gets the Profits? II .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` - Residual claimants have incentives to maximize firm's profits, as this *maximizes their own income* - Entrepreneurs and shareholders are the only participants in production that are *not* guaranteed an income! - Starting and owning a firm is inherently **risky**! ] .pull-right[ .center[  ] ] --- # People Overestimate Profits .center[  ] .source[Source: [American Enterprise Institute](https://www.aei.org/carpe-diem/the-public-thinks-the-average-company-makes-a-36-profit-margin-which-is-about-5x-too-high-part-ii/)] --- # Profits and Entrepreneurship: A Preview .pull-left[ - In markets, production must face the .hi[profit test]: - <span class="hi-purple">Is consumer's willingness to pay `\(>\)` opportunity cost of inputs?</span> - Profits are an indication that **value is being created for society** - Losses are an indication that **value is being destroyed for society** - Survival in markets *requires* firms continually create value & earn profits ] .pull-right[ .center[  ] ] --- # The Firm's Optimization Problem I .pull-left[ - So what do firms do? 1. **Choose:** .hi-blue[ < some alternative >] 2. **In order to maximize:** .hi-green[< profits >] 3. **Subject to:** .hi-red[< technology >] - We've so far assumed they maximize profits and they are limited by their technology ] .pull-right[ .center[  ] ] --- # The Firm's Optimization Problem II .pull-left[ - What do firms **choose**? (Not an easy answer) - Prices? - Depends on the market the firm is operating in! - Study of <span class="hi">industrial organization</span> - Essential question: .hi-turquoise[how competitive is a market?] This will influence what firms (can) do ] .pull-right[ .center[  ] ] --- # Industrial Organization: A Roadmap I .pull-left[ - Begin with one extreme case: .hi[“perfect competition”] - Firms can choose to sell as much `\(q^*\)` as they want - Firms are constrained to sell at the (exogenous) market price `\(\bar{p}\)` - Appropriate for settings with *many* firms, each small relative to market ] .pull-right[ .center[  ] ] --- # Interlude .pull-left[ - After we find firm's .hi-purple[optimal decisions] in this market (and have Exam 2), we will then finally look at .hi-purple[Unit III: Market Equilibrium] - Put .red[Supply] and .blue[Demand] together ] .pull-right[ <img src="2.1-slides_files/figure-html/unnamed-chunk-3-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Interlude .pull-left[ - We've seen how **consumers** cause and respond to market changes - e.g. `\((\Delta p_x\)`, `\(\Delta p_y\)`, `\(\Delta m\)`) - We're about to explore how **producers** cause and respond to market changes - Finally we can explain all of these market changes with Supply and Demand .hi[equilibrium models] - Discuss how markets work, why they are good & efficient, and when they fail ] .pull-right[ <img src="2.1-slides_files/figure-html/unnamed-chunk-4-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Industrial Organization: A Roadmap II .pull-left[ - Examine another extreme case: .hi[monopoly] of a single seller - Appropriate for some markets - .hi-purple[“Imperfect competition”]: models of .hi[monopolistic competition] & .hi[oligopoly] - In latter case, firms act **strategically**, so we will need <span class="hi-purple">game theory</span> - Firms can choose *both* `\(q^*\)` & `\(p^*\)` to maximize `\(\pi\)` ] .pull-right[ .center[  ] ]