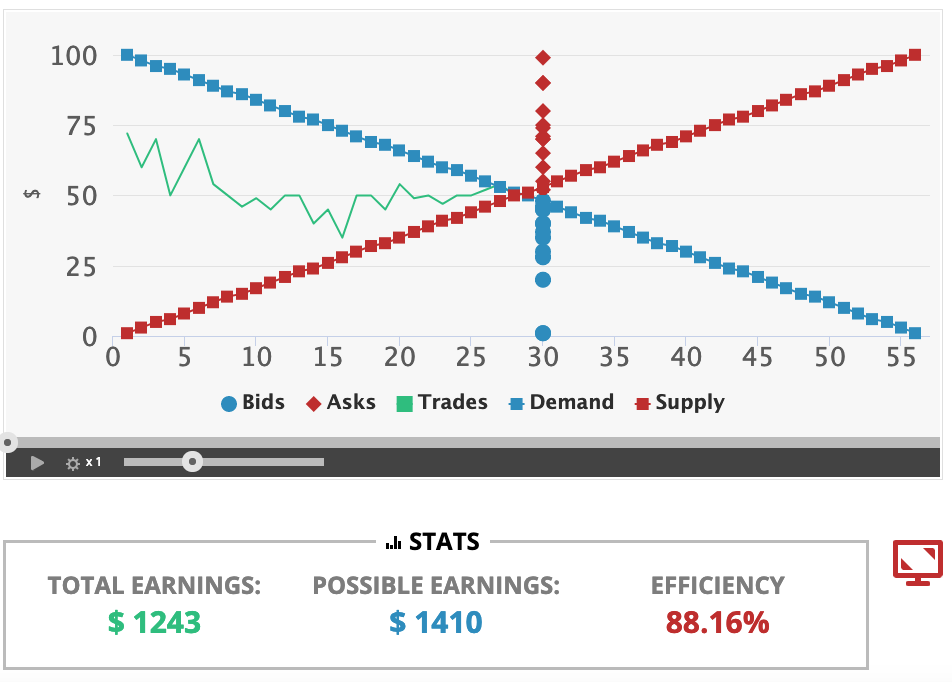

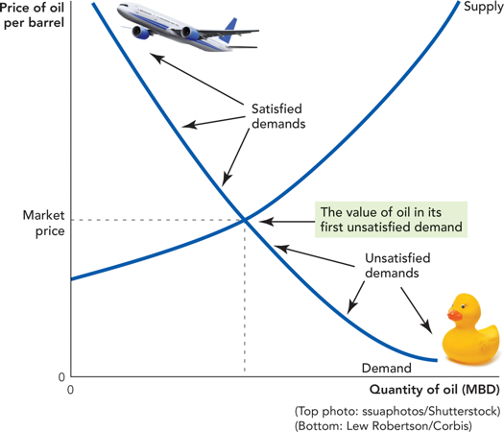

class: title-slide # 3.5 — The *Dynamic* Benefits of Markets ## ECON 306 • Microeconomic Analysis • Spring 2023 ### Ryan Safner<br> Associate Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/microS23"><i class="fa fa-github fa-fw"></i>ryansafner/microS23</a><br> <a href="https://microS23.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>microS23.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Why Markets Tend to Equilibrate, Redux](#7) ### [The Social Functions of Market Prices](#23) ### [Uncertainty and Profits](#37) --- # The Model is Not the Reality I .pull-left[ .center[  ] ] .pull-right[ > *“All models are wrong, but some are useful.”* .smallest[ - This course is about economic modeling and formal theory - Lots of applications beyond this course - Models help us *understand* reality, but they *are not* reality! - Don't mistake the map for the territory itself ] ] --- # The Model is Not the Reality II .pull-left[ .center[  ] ] .pull-right[ .smallest[ - Our models so far have given us interesting results: - Markets reach equilibrium - Economic profits are zero in the long run in competitive markets - Both are **fictional**! - But the models **still** show us useful insights about how a market economy works - Some readings in today’s readings page to help you understand ] ] --- # The Model is Not the Reality III .center[  .source[ Source: [SMBC](https://www.smbc-comics.com/comic/2013-09-19) “Shame on the three of you who enjoyed this joke” ] ] --- # The Model is Not the Reality III .center[  ] --- class: inverse, center, middle # Why Markets Tend to Equilibrate, Redux --- # The Law of One Price I .pull-left[ - .hi[Law of One Price]: *all* units of the *same* good exchanged on the market will tend to have the same market price (the market-clearing price, `\(p^*)\)` ] .pull-right[ <img src="3.4-slides_files/figure-html/unnamed-chunk-1-1.png" width="504" style="display: block; margin: auto;" /> ] --- # The Law of One Price II .pull-left[ .center[  ] ] .pull-right[ .smaller[ - Consider if there are *multiple* different prices for *same* good: - .hi-purple[Arbitrage] opportunities: optimizing individuals recognize **profit opportunity**: - Buy at low price, resell at high price! - There are possible gains from trade or gains from innovation to be had - .hi-purple[Entrepreneurship]: recognizing profit opportunities and entering a market as a seller to try to capture gains from trade/innovation ] ] --- # Arbitrage and Entrepreneurship I .center[  ] --- # Arbitrage and Entrepreneurship II .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/HiB9L3dG-Aw" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # Arbitrage and Entrepreneurship III .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/yGf6LNWY9AI" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # Uncertainty vs. Risk .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/GiPe1OiKQuk" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # Uncertainty vs. Risk .left-column[ .center[  ] ] .right-column[ - **“Known knowns”**: .hi-purple[perfect information] - **“Known unknowns”**: .hi-purple[risk] - We know the probability distribution of states that *could* happen - We just don't know *which* state will be realized - We can estimate probabilities, maximize expected value, minimize variance, etc. ] --- # Uncertainty vs. Risk .left-column[ .center[  ] ] .right-column[ - **“Unknown unknowns”**: .hi[uncertainty] - We don’t even know the probability distribution of states that *could* happen - *No model to optimize* in a world of uncertainty! ] --- # The Role of Entrepreneurial Judgment .left-column[ .center[  ] ] .right-column[ - Under true .hi[uncertainty], it’s not that we can’t assign probabilities to each outcome; we do not even have the knowledge necessary to list all possible outcomes! - Requires .hi-purple[entrepreneurial judgment] to *both*: 1. estimate possible actions *and* 2. estimate the likelihood of their success - .hi[Entrepreneur] is central player, earns pure profits (a residual) for *bearing uncertainty* .source[For more, see Knight 1920 in [today’s readings](/content/3.4-content/#readings).] ] --- # Entrepreneurial Judgment .left-column[ .center[  .smallest[ Henry Ford 1863-1947 ] ] ] .right-column[ > “If I had asked people what they wanted, they would have said **faster horses**.” - Henry Ford ] --- # Entrepreneurial Judgment .pull-left[ .center[  ] ] .pull-right[ > “It's really hard to design products by focus groups. A lot of times, **people don't know what they want until you show it to them**.” - Steve Jobs ] --- # Uncertainty and Entrepreneurship .left-column[ .center[  Mark Zuckerberg 1984- ] ] .right-column[ > "Why were we the ones to build [Facebook]? We were just students. We had way fewer resources than big companies. If they had focused on this problem, they could have done it. The only answer I can think of is: **we just cared more**. **While some doubted** that connecting the world was actually important, **we were building**. While others doubted that this would be sustainable, **we were forming lasting connections**." ] --- # How Markets Get to Equilibrium I .pull-left[ .center[  ] ] .pull-right[ .smaller[ - .hi-turquoise[Nobody knows “the right price” for things] - Each buyer and seller only know **their own** reservation prices - Buyers and sellers adjust their bids/asks - Markets do not *start* competitive, but *become* competitive! - New entrepreneurs enter to try to capture gains from trade/innovation - As these gains are exhausted, prices converge to equilibrium ] ] --- # How Markets Get to Equilibrium II .pull-left[ .center[  ] .source[For more, see Hayek 1945 in [today’s readings](/content/3.4-content/#readings).] ] .pull-right[ .smallest[ - Errors and imperfect information > `\(\implies\)` multiple prices > `\(\implies\)` arbitrage opportunities > `\(\implies\)` entrepreneurship > `\(\implies\)` correcting mistakes > `\(\implies\)` people update their behavior & expectations - Markets are .hi-purple[discovery processes] that *discover* the right prices, the optimal uses of resources, and cheapest production methods, none of which can be known in advance! ] ] --- # How Markets Get to Equilibrium III .pull-left[ .center[  ] ] .pull-right[ .smallest[ - Economy as a .hi[cat]-and-.hi-purple[mouse] game between: - .hi-purple[Mouse]: preferences, technologies, alternative uses of resources - .hi[Cat]: market prices, least-cost technologies - .hi[Cat] always chasing .hi-purple[mouse] - .hi-purple[Mouse] *always* moving - Any time .hi[cat] hasn’t caught .hi-purple[mouse]: profit opportunities - **IF** .hi-purple[mouse] *froze*, market would rest at equilibrium ] ] --- class: inverse, center, middle # The Social Functions of Market Prices --- # Prices are Signals I .center[  ] --- # Prices are Signals II .pull-left[ .center[  ] ] .pull-right[ .smallest[ - .hi-purple[Markets are social *processes* that generate information via prices] - .hi-purple[Prices are never “given”], prices .hi-purple[emerge] dynamically from negotiation and market decisions of entrepreneurs and consumers - **Competition**: is a .hi-purple[discovery process] which *discovers* what consumer preferences are and what technologies are lowest cost, and how to allocate resources accordingly ] .source[For more, see Hayek 1945 in [today’s readings](/content/3.4-content/#readings).] ] --- # The Social Functions of Prices I .pull-left[ .center[  ] ] .pull-right[ .smaller[ A relatively high price: - .hi-purple[Conveys information]: good is relatively scarce - .hi-purple[Creates incentives for]: - **Buyers**: conserve use of this good, seek substitutes - **Sellers**: produce more of this good - **Entrepreneurs**: find substitutes and innovations to satisfy this unmet need ] ] --- # The Social Functions of Prices II .pull-left[  ] .pull-right[ .smaller[ A relatively low price - .hi-purple[Conveys information]: good is relatively abundant - .hi-purple[Creates incentives for]: - **Buyers**: substitute away from expensive goods towards this good - **Sellers**: Produce less of this good, talents better served elsewhere - **Entrepreneurs**: talents better served elsewhere: find more severe unmet needs ] ] --- # The Social Functions of Prices III .pull-left[ .center[  ] ] .pull-right[ .smaller[ - .hi-purple[Prices tell us how to allocate scarce resources among competing uses] - Think of diminishing marginal utility: - allocate scarce good to highest-valued use first - as supply becomes more plentiful (price falls), can allocate more units of the good to lower-valued uses (higher-valued uses already satisfied) ] ] --- class: inverse, center, middle # Uncertainty and Profits --- # Uncertainty, Tacit Information, and Profit I .pull-left[ - **Economic theory**: in a perfectly competitive market, in the long run, economic profit `\(\rightarrow\)` to zero - **Real world**: there *are* often economic profits - Our blackboard models assume perfect information - In reality we have to deal with .hi-purple[uncertainty] ] .pull-right[ .center[  ] ] --- # Uncertainty, Tacit Information, and Profit II .pull-left[ .smaller[ - Imperfect information: mispricing and multiple prices `\(\rightarrow\)` arbitrage/profit opportunities - Some people recognize opportunities ($20 bills) that others do not see - .hi-purple[In a world of certainty, there would be no profit] - The model world of perfect competition is a fictional world of certainty - The real world, *because* it’s uncertain, *has* profit opportunities! ] ] .pull-right[ .center[  ] ] --- # Uncertainty, Tacit Information, and Profit III .pull-left[ .smallest[ - Firms don’t actually *maximize* profits 😨, just a convenient assumption! - In a world of uncertainty (unlike mere risk), there’s no way to *maximize* anything! - Real world is *not* a mere constrained maximization problem! - Better to think in **evolutionary** terms: - Firms that *best* adapt to market circumstances will *survive* and earn profit...whether by skill & talent or just dumb luck! ] ] .pull-right[ .center[  ] ] .source[For more, see Alchian 1950, Gigerenzer, 2012, and Smith, 2003 in [today’s readings](/content/3.4-content/#readings).] --- # Uncertainty, Tacit Information, and Profit IV .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/KUxMY77i0q4" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # Reminder: Profits and Entrepreneurship .pull-left[ .center[  ] ] .pull-right[ .smaller[ - In markets, production faces .hi[profit-test]: - <span class="hi-purple">Is consumer's willingness to pay `\(>\)` opportunity cost of inputs?</span> - Profits are an indication that **value is being created for society** - Losses are an indication that **value is being destroyed for society** - Survival for sellers in markets *requires* firms continually create value and earn profits or die ] ] --- # Why We Need Prices, Profits, and Losses I .pull-left[ .center[  ] ] .pull-right[ .smaller[ - People often confuse the .hi[economic problem] with a .hi-purple[technological problem] - .hi-purple[Technological problem]: how to allocate scarce resources to accomplish a particular goal - e.g. buy the right combination of goods to maximize utility - e.g. buy the right combination of inputs and produce output to maximize profits - given stable prices, preferences, and technologies, **a computer can solve this problem** ] .source[For more, see Hayek 1945 in [today’s readings](/content/3.4-content/#readings).] ] --- # Why We Need Prices, Profits, and Losses II .pull-left[ .center[  ] ] .pull-right[ - .hi[Economic calculation problem]: how to determine which of the infinite technologically-feasible options are *economically* viable? - .hi-purple[How to best make use of dispersed knowledge to coordinate conflicting plans of individuals for their own ends?] - ONLY can be **discovered** through competition, prices, profits & losses .source[For more, see Hayek 1945 in [today’s readings](/content/3.4-content/#readings). ] ] --- # What if there Were No Prices? I .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/zkPGfTEZ_r4" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # What if there Were No Prices? II .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/QwqnRYPcrl0" frameborder="0" allow="accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # For More On The Socialist Calculation Debate .pull-left[ .center[  ] ] .pull-right[ See lesson 4.2 in my History of Economic Thought Course: [The Socialist Calculation Debate](https://thoughtf20.classes.ryansafner.com/schedule) ] --- # And How Did The Soviet Union “Work” For So Long? .pull-left[ .center[  ] ] .pull-right[ See lesson 12 in my Economics of Development Course: [Russia and the Post-Communist Transition](https://devf19.classes.ryansafner.com/schedule) ]